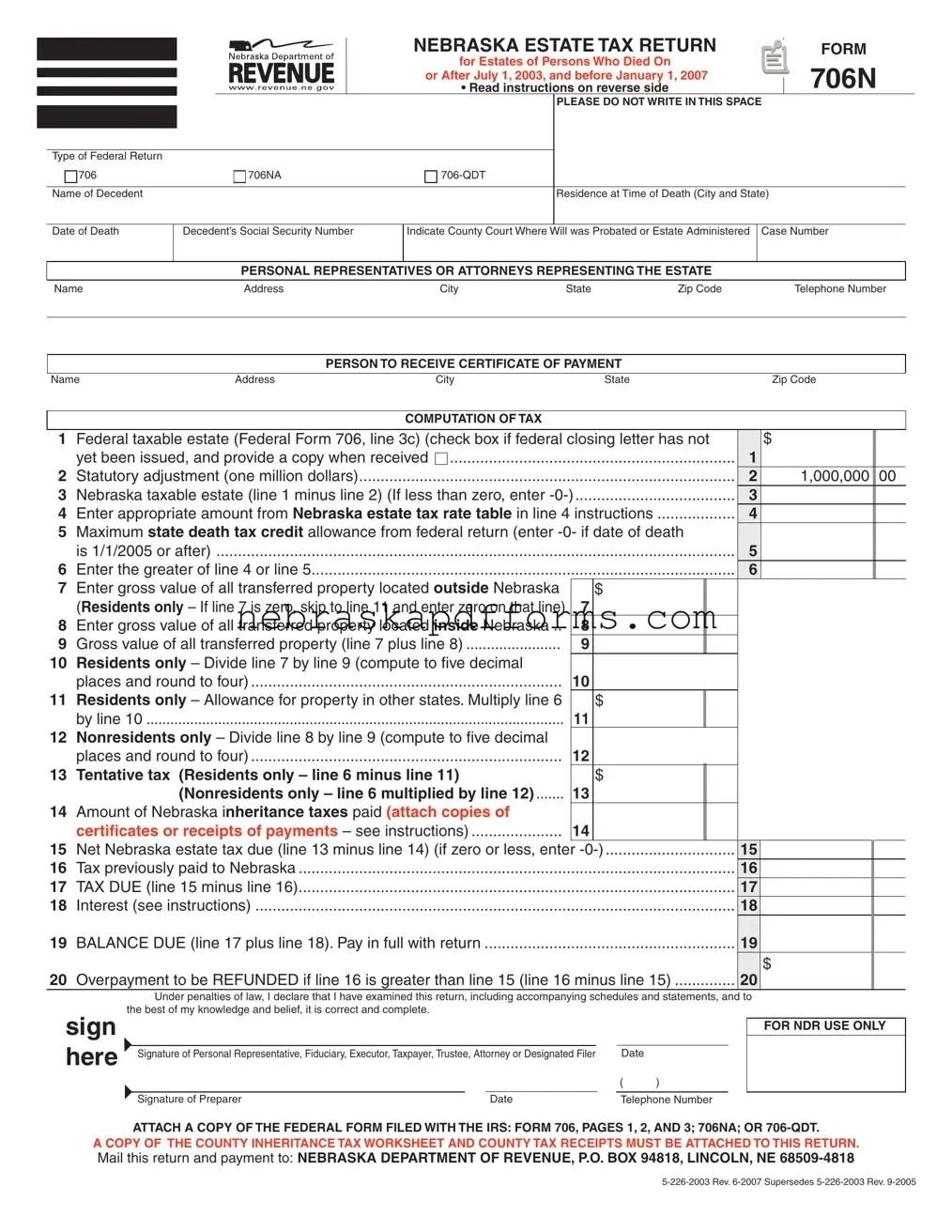

Nebraska 706N Form

The Nebraska 706N form serves as the official estate tax return for individuals who passed away between July 1, 2003, and January 1, 2007. This form is essential for estates with a federal taxable estate of one million dollars or more, regardless of whether a federal return is required. The 706N form collects vital information about the decedent, including their name, date of death, and Social Security number, as well as the county court where the will was probated. Personal representatives or attorneys representing the estate must provide their contact information as well. The form also includes a detailed computation section where the Nebraska taxable estate is calculated, taking into account the federal taxable estate and applicable adjustments. Furthermore, it outlines the tax due, including any overpayments and the necessary steps for obtaining a refund if applicable. It is important to note that the completed form must be filed with the Nebraska Department of Revenue within 12 months of the decedent's death, along with any required federal forms and documentation. Understanding the Nebraska 706N form is crucial for ensuring compliance with state tax obligations and facilitating the proper administration of the estate.

Document Preview Example

NEBRASKAESTATETAXRETURN

forEstatesofPersonsWhoDiedOn

orAfterJuly1,2003,andbeforeJanuary1,2007

•Readinstructionsonreverseside

FORM

706N

PLEASEDONOTWRITEINTHISSPACE

TypeofFederalReturn

|

706 |

706NA |

|

|

|

|

|

NameofDecedent |

|

ResidenceatTimeofDeath(CityandState) |

|

DateofDeath

Decedent’sSocialSecurityNumber

IndicateCountyCourtWhereWillwasProbatedorEstateAdministered CaseNumber

|

PERSONALREPRESENTATIVESORATTORNEYSREPRESENTINGTHEESTATE |

|

|||

|

|

|

|

|

|

Name |

Address |

City |

State |

ZipCode |

TelephoneNumber |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PERSONTORECEIVECERTIFICATEOFPAYMENT |

|

|

|

|

Name |

Address |

City |

State |

|

ZipCode |

|

|

|

|

|

|

|

|

|

|

COMPUTATIONOFTAX |

|

|

|

|

|

|

|

|||

1 Federaltaxableestate(FederalForm706,line3c)(checkboxiffederalclosingletterhasnot |

|

$ |

||||

|

yetbeenissued,andprovideacopywhenreceived |

1 |

|

|||

|

.......................................................................................2 Statutoryadjustment(onemilliondollars) |

2 |

1,000,000 00 |

|||

|

.....................................3 |

3 |

|

|||

|

..................4 EnterappropriateamountfromNebraskaestatetaxratetableinline4instructions |

4 |

|

|||

5

|

is1/1/2005orafter) |

5 |

|

|

..................................................................................................6 Enterthegreaterofline4orline5 |

6 |

|

|

7 EntergrossvalueofalltransferredpropertylocatedoutsideNebraska |

$ |

|

|

8 EntergrossvalueofalltransferredpropertylocatedinsideNebraska.. |

|

8 |

|

9 Grossvalueofalltransferredproperty(line7plusline8) |

|

9 |

10

|

placesandroundtofour) |

|

10 |

|

11 |

$ |

|

|

byline10 |

11 |

|

12

|

placesandroundtofour) |

12 |

|

|

|

|

|

||

|

13 Tentativetax |

|

$ |

|

|

|

|

|

|

|

|

13 |

|

|

|

|

|

||

14 AmountofNebraskainheritancetaxespaid(attachcopiesof |

|

|

|

|

|

|

|

||

|

|

14 |

|

|

|

|

|

||

|

15 NetNebraskaestatetaxdue(line13minusline14)(ifzeroorless,enter |

|

|

15 |

|

|

|||

|

.....................................................................................................16 TaxpreviouslypaidtoNebraska |

|

|

|

16 |

|

|

||

|

.....................................................................................................17 TAXDUE(line15minusline16) |

|

|

|

17 |

|

|

||

|

...............................................................................................................18 Interest(seeinstructions) |

|

|

|

18 |

|

|

||

|

19 BALANCEDUE(line17plusline18).Payinfullwithreturn |

|

|

|

19 |

|

|

||

|

20 OverpaymenttobeREFUNDEDifline16isgreaterthanline15(line16minusline15) |

20 |

$ |

|

|||||

|

|

||||||||

sign here

Underpenaltiesoflaw,IdeclarethatIhaveexaminedthisreturn,includingaccompanyingschedulesandstatements,andto thebestofmyknowledgeandbelief,itiscorrectandcomplete.

FORNDRUSEONLY

SignatureofPersonalRepresentative,Fiduciary,Executor,Taxpayer,Trustee,AttorneyorDesignatedFiler |

|

Date |

||

|

|

|

|

( ) |

|

|

|

|

|

SignatureofPreparer |

|

Date |

TelephoneNumber |

|

ACOPYOFTHECOUNTYINHERITANCETAXWORKSHEETANDCOUNTYTAXRECEIPTSMUSTBEATTACHEDTOTHISRETURN.

INSTRUCTIONS |

||

WHOMUSTFILE.This return must be filed for estates with a federal |

or his or her successors or assigns is entitled to a refund of the amount |

|

taxable estate of one million dollars or more, whether or not required to |

of overpayment plus interest. |

|

file Federal Forms 706, 706NA, or |

Interest on refunds will be calculated at the statutory rate. |

|

on or after July 1, 2003, and before January 1, 2007, and was a resident |

SPECIFICINSTRUCTIONS |

|

of Nebraska, or owned real property in Nebraska, at the time of death. |

||

|

||

Estates of persons who died on or after January 1, 2003, but before July 1, 2003, should use Nebraska Form

WHENANDWHERETOFILE.This return is due 12 months after the date of death of the decedent. This return is to be filed with the Nebraska Department of Revenue, P.O. Box 94818, Lincoln, Nebraska

HAVEQUESTIONS?Check our Web site: www.revenue.ne.gov or call

AMOUNTOFTAX.The amount of estate tax due the state of Nebraska begins with the greater of two amounts. The first amount is the maxi- mum state tax credit allowance upon the tax imposed by Chapter 11 of the Internal Revenue Code. (Note: This allowance has been completely phased out on the federal return for decedents with dates of death after December 31, 2004.) The second amount is the Nebraska taxable estate (federal taxable estate [Federal Form 706 line 3c] minus one million dollars) multiplied by the tax rates in the Nebraska estate tax table — see line 4 instructions. Certain adjustments are allowed as reflected in lines 7 through 14. The net Nebraska estate tax due as a result of these calcula- tions is entered on line 15.

INTEREST.If the tax due as computed on line 15 of this return is not paid by the prescribed due date, interest on the unpaid tax will be assessed at the statutory rate from the due date until payment is received. The rate of interest may be adjusted on January 1 of every

FEDERALRETURNS. Attach to this return a copy of Federal Form 706 (pages 1, 2, and 3), 706NA, or

FEDERAL CLOSING LETTER. If a federal return is required to be filed attach a copy of the Internal Revenue Service or federal court determination of estate tax, i.e., the federal closing letter which sets out the federal estate tax liability. If the determination is unavailable, the box on line 1 must be checked. When the closing letter is issued by the Internal Revenue Service or the federal court, a copy of the determination must be filed with the Nebraska Department of Revenue by the personal representative within ten days of receipt.

CERTIFICATEEVIDENCINGPAYMENT.A certificate evidencing payment of Nebraska estate tax will be issued after the Nebraska Estate Tax Return has been filed and the tax paid. The Nebraska Estate Tax Return has not been properly filed until the federal closing letter (if any) and certificates or receipts evidencing tax payments to other states or political subdivisions have been provided.

INHERITANCETAXWORKSHEET.Attach a copy of the inheritance tax worksheet filed with the appropriate Nebraska county court.

AMENDEDRETURN.If the amount of Nebraska tax due is affected by a change made by the Internal Revenue Service or otherwise by the filing of an amended federal return, then an amended Nebraska return must be filed. Complete Form 706N, mark it “Amended” at the top of the return, and attach a copy of the dated notice of change from the Internal Revenue Service or a copy of the amended federal return.

REFUNDOFOVERPAYMENT.An overpayment of tax to the state of Nebraska will be refunded upon the filing of an amended return. The claim for refund must be filed with the department within four years after the date of overpayment, or within one year of a change in the amount of federal tax due, whichever is later. The party making such overpayment

|

Nebraskataxableestate |

|

|

|

OfExcess |

|||

|

fromline3 |

|

|

|

|

|

Over |

|

|

Atleast |

Butlessthan |

|

Tax= |

+ % |

|

|

|

$ |

0 |

$ |

100,000 |

$ |

0 |

5.6 |

$ |

0 |

|

100,000 |

|

500,000 |

|

5,600 |

6.4 |

|

100,000 |

|

500,000 |

|

1,000,000 |

|

31,200 |

7.2 |

|

500,000 |

|

1,000,000 |

|

1,500,000 |

|

67,200 |

8.0 |

|

1,000,000 |

|

1,500,000 |

|

2,000,000 |

|

107,200 |

8.8 |

|

1,500,000 |

|

2,000,000 |

|

2,500,000 |

|

151,200 |

9.6 |

|

2,000,000 |

|

2,500,000 |

|

3,000,000 |

|

199,200 |

10.4 |

|

2,500,000 |

|

3,000,000 |

|

3,500,000 |

|

251,200 |

11.2 |

|

3,000,000 |

|

3,500,000 |

|

4,000,000 |

|

307,200 |

12.0 |

|

3,500,000 |

|

4,000,000 |

|

5,000,000 |

|

367,200 |

12.8 |

|

4,000,000 |

|

5,000,000 |

|

6,000,000 |

|

495,200 |

13.6 |

|

5,000,000 |

|

6,000,000 |

|

7,000,000 |

|

631,200 |

14.4 |

|

6,000,000 |

|

7,000,000 |

|

8,000,000 |

|

775,200 |

15.2 |

|

7,000,000 |

|

8,000,000 |

|

9,000,000 |

|

927,200 |

16.0 |

|

8,000,000 |

|

9,000,000 |

|

|

1,087,200 |

16.8 |

|

9,000,000 |

|

LINE7.Enter the gross value of the transferred property located outside Nebraska.

For a resident decedent, this is the value of real estate and tangible personal property located outside of Nebraska.

For a nonresident decedent, this is the entire value of his or her estate, less the value of any interest in Nebraska real estate and tangible personal property located within Nebraska. Intangibles held in Nebraska at the time of a nonresident’s death are to be valued at their fair market value and included on line 7.

Residentsonly – If the gross value of the transferred property located outside Nebraska is zero, skip to line 11 and enter zero on that line. If line 7 is greater than zero, however, complete lines 8 through 10 before proceeding to line 11. Use line 9 instructions for assistance in determining the appropriate gross value amounts.

LINE8. Enter the gross value of all transferred property within Nebraska. This includes a nonresident decedent’s interest in Nebraska real estate and tangible personal property.

LINE9.Enter the gross value of all transferred property. This amount is the total gross estate reported on the federal return. This gross amount is prior to any adjustments for expenses or any other allowable deductions used in computing the taxable estate.

LINE14.Attach a copy of the county inheritance tax worksheet and copies of receipts or certificates evidencing payment of inheritance tax.

LINE 19. Attach a check or money order payable to the Nebraska Department of Revenue for the sum reported on line 19.

SIGNATURES.A personal representative, fiduciary, executor, taxpayer, trustee, attorney, or designated filer of the estate must sign this return. An attorney must indicate the state wherein currently qualified to practice law. If another person is authorized to sign this return, there must be a power of attorney on file with the department.

Any person who is paid for preparing this return must also sign the return as preparer.

File Information

| Fact Name | Details |

|---|---|

| Form Purpose | The Nebraska 706N form is used for filing estate taxes for individuals who died between July 1, 2003, and January 1, 2007. |

| Filing Requirement | This form must be filed if the federal taxable estate is one million dollars or more, regardless of whether a federal return is required. |

| Governing Law | The Nebraska 706N form is governed by the Nebraska Revised Statutes, Chapter 77, specifically sections related to estate taxes. |

| Filing Deadline | The return is due 12 months after the date of the decedent's death. |

| Tax Calculation | The Nebraska estate tax is calculated based on the Nebraska taxable estate, which is the federal taxable estate minus one million dollars. |

| Payment Instructions | Payments should be sent to the Nebraska Department of Revenue at P.O. Box 94818, Lincoln, NE 68509-4818. |

| Required Attachments | Attach a copy of the federal Form 706 and any applicable county inheritance tax worksheets and receipts. |

Other PDF Templates

Nebraska Fuel Tax - Applicants must provide equipment details where the fuel was utilized, including make, model, and whether the equipment is licensed, to support their claim on Form 84AG.

For those planning ahead, the Colorado Do Not Resuscitate Order is crucial in ensuring your healthcare preferences are honored. You can find more information and access the form at the following link: necessary Do Not Resuscitate Order details.

Ne Form 13 - This form facilitates a seamless transition to a new business name, minimizing confusion for customers and clients.