Nebraska 51C Form

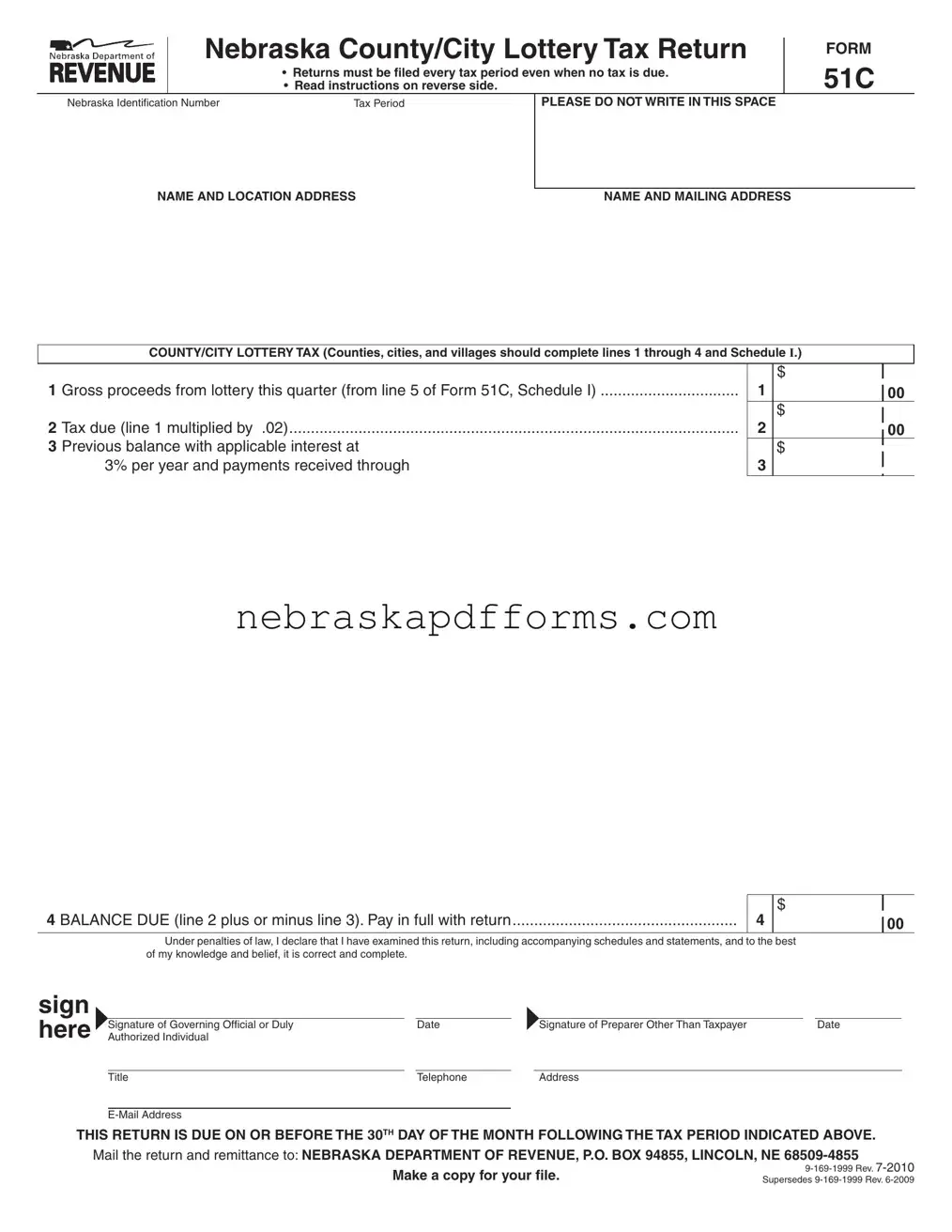

The Nebraska 51C form, officially known as the County/City Lottery Tax Return, serves a critical role in the financial oversight of lottery operations within the state. Every county, city, or village that conducts a lottery must submit this form for each tax period, regardless of whether any tax is owed. The form requires detailed reporting of gross lottery proceeds, calculated at a tax rate of two percent. Additionally, it includes provisions for previous balances, interest, and penalties for late filings. The return must be filed by the 30th day of the month following the end of the tax period, ensuring timely compliance with state regulations. It is essential for organizations to use the pre-identified version of the form, as photocopies or incorrect versions will not be accepted. Signatures from authorized officials are mandatory, and a thorough understanding of the accompanying instructions is necessary to avoid penalties and ensure accurate reporting. Failure to comply can lead to significant repercussions, including potential license suspension or revocation. This article will explore the intricacies of the Nebraska 51C form, providing insights into its requirements and implications for local governments engaged in lottery activities.

Document Preview Example

Nebraska County/City Lottery Tax Return

• Returns must be filed every tax period even when no tax is due. • Read instructions on reverse side.

FORM

51C

Nebraska Identification Number |

Tax Period |

PLEASE DO NOT WRITE IN THIS SPACE

NAME AND LOCATION ADDRESS |

NAME AND MAILING ADDRESS |

COUNTY/CITY LOTTERY TAX (Counties, cities, and villages should complete lines 1 through 4 and Schedule I.)

1 Gross proceeds from lottery this quarter (from line 5 of Form 51C, Schedule I) ................................

2 Tax due (line 1 multiplied by .02)........................................................................................................

3 Previous balance with applicable interest at

3% per year and payments received through

|

$ |

1 |

00 |

|

|

|

$ |

2 |

00 |

|

$ |

3 |

|

|

|

4 BALANCE DUE (line 2 plus or minus line 3). Pay in full with return ....................................................

4

$

00

Under penalties of law, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is correct and complete.

sign here

|

|

|

|

|

|

|

Signature of Governing Official or Duly |

|

Date |

|

Signature of Preparer Other Than Taxpayer |

|

Date |

Authorized Individual |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Title |

Telephone |

Address |

THIS RETURN IS DUE ON OR BEFORE THE 30TH DAY OF THE MONTH FOLLOWING THE TAX PERIOD INDICATED ABOVE.

Mail the return and remittance to: NEBRASKA DEPARTMENT OF REVENUE, P.O. BOX 94855, LINCOLN, NE

Make a copy for your file. |

||

Supersedes |

||

|

INSTRUCTIONS

WHO MUST FILE. Every county, city, or village licensed to conduct a lottery must ile this return. A return is required for every tax period, or portion of a tax period, from each county, city, or village licensed even when no tax is due.

WHEN AND WHERE TO FILE. This return, properly signed, with a check payable to the Nebraska Department of Revenue for the balance reported on line 4, is considered timely iled if postmarked on or before the 30th day of the month following the end of the tax period covered by the return. Mail to the Nebraska Department of Revenue, P.O. Box 94855, Lincoln, Nebraska

Counties, cities, and villages licensed to conduct a lottery must ile Nebraska Schedule I – County/City Lottery Activity Report with this return.

PREIDENTIFIED RETURN. This return must be used only by the licensed organization whose name is printed on it. Do not ile returns which are photocopies, are for another tax period, or have not been preidentiied. If you have not received a return for the tax period, and will be iling a paper return, request a duplicate from the Charitable Gaming Division, or visit our website at www.revenue.ne.gov/gaming to print a Form 51C. Complete the ID number, tax period, name, and address information.

PENALTY AND INTEREST. In the event that the return is not iled by the prescribed due date, a penalty will be assessed in the amount of ten percent of the tax not paid by the due date, or $25, whichever is greater. Interest on any unpaid tax will be assessed at the rate speciied in Neb. Rev. Stat. §

VERIFICATION AND AUDIT. Records to substantiate this return must be kept available for a period of at least three years following the date of iling the return.

SPECIFIC INSTRUCTIONS

LINE 1. Counties, cities, and villages are required to remit a two percent tax on all gross proceeds from the conduct of a lottery. Enter line 5 from Nebraska Schedule I – County/City Lottery Activity Report.

LINE 2. Multiply line 1 by the state tax rate indicated. This is the amount of county/city lottery tax due to the Department for this tax period.

LINE 3. A balance due or credit resulting from a partial payment, mathematical or clerical error, penalty, or interest relating to prior returns will be entered in this space by the Department. The amount of interest includes interest on unpaid tax through the due date of this return. If the amount due is paid before the due date, the interest will be recomputed, and a credit will be given on your next return. If the amount entered has been satisied by a previous remittance, it should be disregarded when computing the amount to remit on line 4. If a credit is shown, it may be applied to the current tax liability.

LINE 4. Attach a check made payable to the Nebraska Department of Revenue for the amount reported on line 4. Checks may be presented for payment electronically.

AUTHORIZED SIGNATURE. This return must be signed by a governing oficial or other duly authorized individual. A person who is paid for preparing this return must also sign the return as a preparer.

Any questions regarding the completion of the Nebraska County/City Lottery Tax Return, Form 51C, should be addressed to the Nebraska Department of Revenue, Charitable Gaming Division, P.O. Box 94855, Lincoln, Nebraska

File Information

| Fact Name | Details |

|---|---|

| Filing Requirement | Every county, city, or village licensed to conduct a lottery must file Form 51C for each tax period, even if no tax is due. |

| Due Date | The return is due on or before the 30th day of the month following the end of the tax period. |

| Governing Law | This form is governed by Nebraska Revised Statutes, specifically Neb. Rev. Stat. § 45-104.02. |

| Penalty for Late Filing | A penalty of 10% of the unpaid tax or $25, whichever is greater, will be assessed if the return is filed late. |

| Record Keeping | Records supporting the return must be kept for at least three years from the filing date. |

Other PDF Templates

Form 941 - Details the information required from both the withholding entity and the nonresident individual.

Nebraska Sales Tax Form 6 - Guides on computing the tax base by deducting trade-in values and manufacturer rebates from the total sales price.

For those seeking clarity on medical decisions, the Colorado Do Not Resuscitate Order is an indispensable document that articulates the choice to forego cardiopulmonary resuscitation. You can find more information and access the necessary form through this helpful resource: vital Do Not Resuscitate Order guidelines.

Nebraska State Tax Form - A tool for Nebraska enterprises to request changes in filing frequency for various state taxes including sales and use tax.