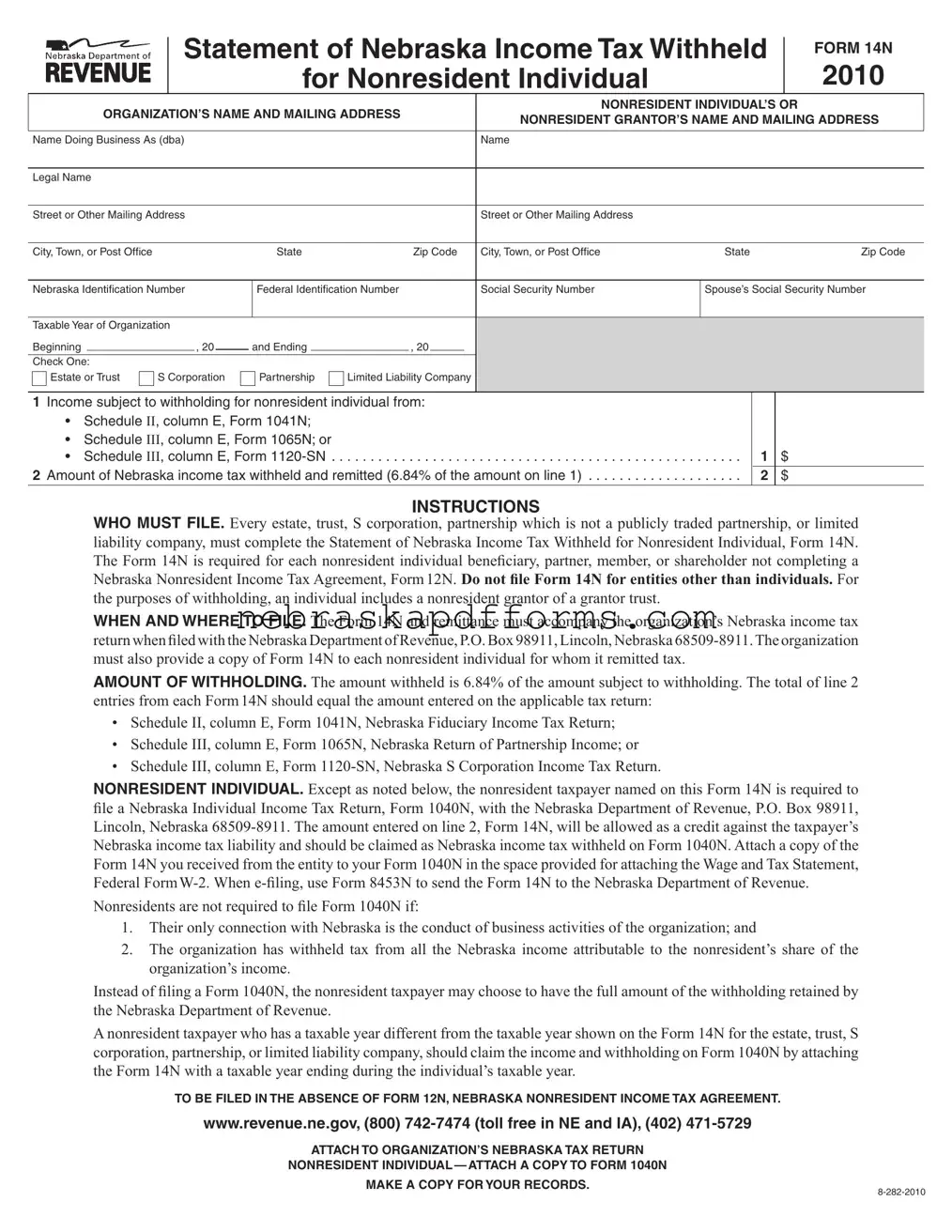

Nebraska 14N Form

The Nebraska 14N form, officially known as the Statement of Nebraska Income Tax Withheld for Nonresident Individual, serves a crucial role in the state's tax system. Designed for use by estates, trusts, S corporations, partnerships, and limited liability companies, this form ensures that nonresident individuals who receive income from these entities are accurately accounted for in terms of tax withholding. Specifically, the form captures essential information such as the names and addresses of both the organization and the nonresident individual, along with their respective identification numbers. It also outlines the amount of Nebraska income tax withheld, which is calculated at a rate of 6.84% of the income subject to withholding. Importantly, the 14N must be filed alongside the organization's Nebraska income tax return and a copy provided to each nonresident individual for whom tax has been remitted. Furthermore, nonresident individuals are required to file a Nebraska Individual Income Tax Return, allowing them to claim the withheld amount as a credit against their tax liability. This form is particularly significant for those who do not complete a Nebraska Nonresident Income Tax Agreement, ensuring compliance with state tax obligations while providing a streamlined process for both organizations and nonresident taxpayers.

Document Preview Example

Statement of Nebraska Income Tax Withheld

for Nonresident Individual

FORM 14N

2010

|

ORGANIZATION’S NAME AND MAILING ADDRESS |

|

|

|

|

NONRESIDENT INDIVIDUAL’S OR |

|

||||||||

|

|

|

|

NONRESIDENT GRANTOR’S NAME AND MAILING ADDRESS |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name Doing Business As (dba) |

|

|

|

|

|

|

Name |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Street or Other Mailing Address |

|

|

|

|

|

|

Street or Other Mailing Address |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, Town, or Post Office |

|

|

|

|

State |

|

Zip Code |

City, Town, or Post Office |

|

State |

Zip Code |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Nebraska Identification Number |

Federal Identification Number |

|

|

|

Social Security Number |

|

Spouse’s Social Security Number |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable Year of Organization |

|

|

|

|

|

|

|

|

|

|

|||||

Beginning |

|

|

, 20 |

|

|

and Ending |

|

|

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Check One: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Estate or Trust |

S Corporation |

Partnership |

Limited Liability Company |

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Income subject to withholding for nonresident individual from: |

||

|

|

• ScheduleII, column E, Form 1041N; |

|

|

|

• |

Schedule III, column E, Form 1065N; or |

|

|

• |

Schedule III, column E, Form |

2 |

Amount of Nebraska income tax withheld and remitted (6.84% of the amount on line 1) |

||

1$

2$

INSTRUCTIONS

WHO MUST FILE. Every estate, trust, S corporation, partnership which is not a publicly traded partnership, or limited liability company, must complete the Statement of Nebraska Income Tax Withheld for Nonresident Individual, Form 14N.

The Form 14N is required for each nonresident individual beneiciary, partner, member, or shareholder not completing a Nebraska Nonresident Income Tax Agreement, Form 12N. Do not ile Form 14N for entities other than individuals. For the purposes of withholding, an individual includes a nonresident grantor of a grantor trust.

WHEN AND WHERE TO FILE. The Form 14N and remittance must accompany the organization’s Nebraska income tax return when iled with the Nebraska Department of Revenue, P.O. Box 98911, Lincoln, Nebraska

must also provide a copy of Form 14N to each nonresident individual for whom it remitted tax.

AMOUNT OF WITHHOLDING. The amount withheld is 6.84% of the amount subject to withholding. The total of line 2

entries from each Form14N should equal the amount entered on the applicable tax return:

•Schedule II, column E, Form 1041N, Nebraska Fiduciary Income Tax Return;

•Schedule III, column E, Form 1065N, Nebraska Return of Partnership Income; or

•Schedule III, column E, Form

NONRESIDENT INDIVIDUAL. Except as noted below, the nonresident taxpayer named on this Form 14N is required to ile a Nebraska Individual Income Tax Return, Form 1040N, with the Nebraska Department of Revenue, P.O. Box 98911, Lincoln, Nebraska

Nonresidents are not required to ile Form 1040N if:

1.Their only connection with Nebraska is the conduct of business activities of the organization; and

2.The organization has withheld tax from all the Nebraska income attributable to the nonresident’s share of the organization’s income.

Instead of iling a Form 1040N, the nonresident taxpayer may choose to have the full amount of the withholding retained by the Nebraska Department of Revenue.

A nonresident taxpayer who has a taxable year different from the taxable year shown on the Form 14N for the estate, trust, S corporation, partnership, or limited liability company, should claim the income and withholding on Form 1040N by attaching the Form 14N with a taxable year ending during the individual’s taxable year.

TO BE FILED IN THE ABSENCE OF FORM 12N, NEBRASKA NONRESIDENT INCOME TAX AGREEMENT.

www.revenue.ne.gov, (800)

ATTACH TO ORGANIZATION’S NEBRASKA TAX RETURN

NONRESIDENT INDIVIDUAL — ATTACH A COPY TO FORM 1040N

MAKE A COPY FOR YOUR RECORDS.

File Information

| Fact Name | Details |

|---|---|

| Form Purpose | The Nebraska 14N form is used to report income tax withheld for nonresident individuals, including beneficiaries of estates, trusts, and certain business entities. |

| Governing Law | This form is governed by Nebraska Revised Statutes, particularly sections related to income tax withholding for nonresidents. |

| Who Must File | Estates, trusts, S corporations, partnerships (excluding publicly traded partnerships), and limited liability companies must file this form for each nonresident individual. |

| Filing Requirements | The form must be filed along with the organization’s Nebraska income tax return and a copy must be provided to each nonresident individual for whom tax was remitted. |

| Withholding Rate | The withholding rate on income subject to tax is set at 6.84% of the amount reported on the applicable schedules. |

| Tax Credit | The amount withheld can be claimed as a credit against the nonresident individual’s Nebraska income tax liability on Form 1040N. |

| Exemptions | Nonresidents may not need to file Form 1040N if their only connection to Nebraska is through the organization’s business activities and all taxes have been withheld. |

| Record Keeping | It is essential for both the organization and the nonresident individual to keep copies of the Form 14N for their records. |

Other PDF Templates

Nebraska Dmv Bill of Sale - Applicants use the Nebraska DLB 1A form to officially declare their dealership type, whether it's for selling new or used motorcycles, trailers, or a combination of motor vehicles and trailers.

Understanding the importance of a legal document such as the New York Bill of Sale is crucial for anyone involved in a personal property transaction. This form serves to transfer ownership securely, detailing the item description, purchase price, and party names for both buyer and seller. For those in need of a reliable template, Top Forms Online offers a straightforward solution that can ensure all necessary information is documented appropriately.

Are Blue Lights on Cars Illegal - Addresses the procedural requirements for adopting electronic traffic control aids in Nebraska.